Modern Portfolio Theory: Maximizing Efficiency in Global Wealth Management

Modern Portfolio Theory: Maximizing Efficiency in Global Wealth Management

Achieving true wealth preservation requires moving past traditional asset picking. For sophisticated investors, structural diversification is the ultimate tool for risk management. Modern Portfolio Theory (MPT) provides the mathematical framework that underpins this approach.

Introduced by Nobel Laureate Harry Markowitz, MPT transformed how global wealth is managed. It shifted the focus from analyzing individual stocks in isolation to evaluating how assets behave in relation to one another within a unified portfolio. For executives, business owners, and expatriates with substantial wealth, MPT is not just an abstract concept. It serves as the foundational architecture used to construct resilient, tax-optimized, and globally diversified portfolios.

The Core Mechanics: Risk, Return, and the Efficient Frontier

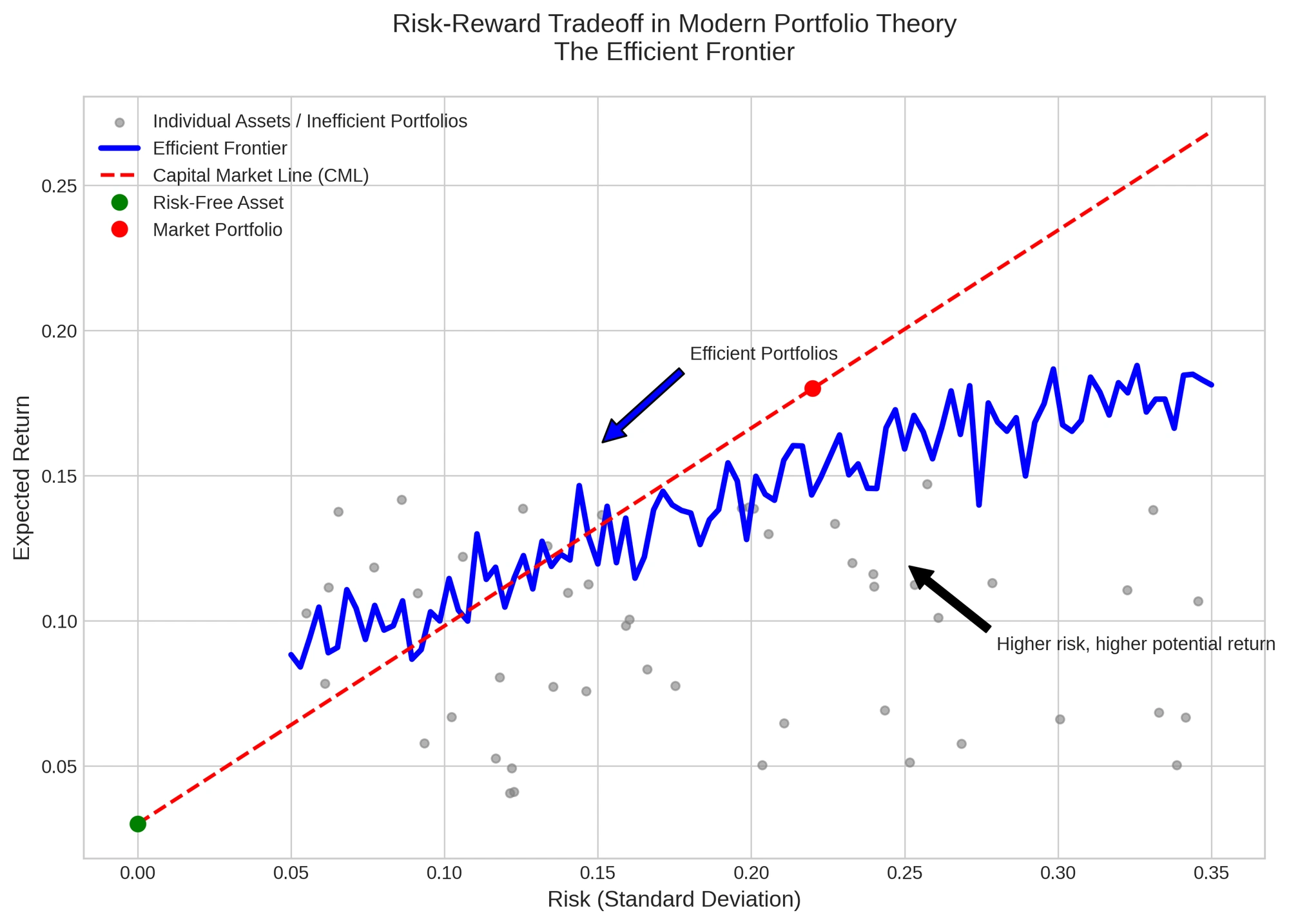

At its core, MPT operates on a simple premise: an asset’s risk and return should not be assessed on their own, but by how they contribute to an overall portfolio’s risk and return profile.

MPT introduces three critical pillars to portfolio construction:

- The Expected Return: The weighted average of all potential returns an asset or portfolio can generate under varying market conditions.

- Volatility as Risk: MPT quantifies risk using standard deviation—measuring how much an asset’s price fluctuates from its historical average.

- The Efficient Frontier: The mathematical sweet spot. It represents a curve of optimal portfolios that offer the highest possible expected return for a specific level of risk, or the lowest risk for a targeted return.

Correlation: The Secret to True Diversification

True diversification is not achieved simply by owning many different assets. It relies on buying assets with low or negative correlation. Correlation is measured on a scale from -1.0 to +1.0. A correlation of +1.0 means two assets move in perfect tandem. A correlation of -1.0 means they move in opposite directions.

If your portfolio consists entirely of European blue-chip stocks and UK equities, your holdings are highly correlated. During a market downturn, they will likely decline together.

MPT proves that adding a low-correlation asset—such as private equity—can actually lower your overall portfolio risk while maintaining or increasing your expected return. By evaluating these mathematical relationships from our Tokyo headquarters, we help you source alternative global assets that break traditional correlation traps.

Applying MPT to the Global Expatriate Lifestyle

For cross-border professionals and expatriates in their peak earning years, standard MPT models must be adjusted to account for real-world complexities like currency exposure and multi-jurisdictional tax liabilities.

When we apply MPT to your wealth, we expand the theory to address three critical cross-border variables:

Dual-Currency Optimization

Living in Zurich or Milan while holding sterling or US dollar assets introduces severe currency volatility. We view currency as an independent asset class within the MPT framework. We advise on structural overlays and global equity allocations to ensure shifting exchange rates do not push your portfolio off the Efficient Frontier.

The Illiquidity Premium of Private Equity

Traditional MPT assumes all assets can be bought and sold instantly. However, late-stage private equity placements require locking up capital over longer cycles. We adapt the theory by structuring your liquid stock sleeve to serve as an accessible cash-flow buffer. This allows you to harvest the higher returns of illiquid investments without facing sudden cash shortfalls.

Tax and Estate Structuring Wrappers

A portfolio that is mathematically efficient on paper can be severely impacted by French wealth taxes or UK capital gains exposure. True modern portfolio management requires combining asset allocation with structural legal engineering. By utilizing international trusts or specialized insurance structures, we ensure your optimal investment mix remains highly efficient after accounting for international taxes.

The Advisor-Led Advisory Model: Powering Informed Autonomy

Many institutional firms use MPT as a justification to demand full discretionary control over your wealth, managing your funds through automated algorithms. We take a different approach.

We believe that executives, professionals and business owners value control and intellectual autonomy. Our framework uses MPT as an advisory roadmap, not an automated mandate. Our advisors handle the complex quantitative modeling, stress-test correlations across global markets, and present vetted allocations. You retain absolute final veto power over every single asset addition and transaction.

This collaborative approach combines quantitative, institutional-grade science with your ultimate executive authority.

Move Closer to the Efficient Frontier

If you want to analyze how your current holdings stack up, let us know:

- Your current asset split between liquid stocks, cash, and private assets

- Your primary base currency and where you plan to retire

- Any concentrated stock exposure you currently hold from business ownership or corporate equity packages

We can help you audit your portfolio’s correlation risks and map a clear path to optimal efficiency.

Our latest insights